Thank you, Dr. Tkac, for your kind words and for the opportunity to talk to this group.1 It is always wonderful to be back in Georgia and here at the Federal Reserve Bank of Atlanta. And it is an honor to speak at a conference co-organized by the University of Virginia, where I received my Ph.D.

You have heard already today about financial markets and the banking system. To add to that picture, I would like to share with you my outlook for the U.S. economy and my views of appropriate monetary policy. But before that, I want to touch on the importance of central bank communications, and particularly the evolution of Fed communications.

The Value of Communications

One of the reasons I so appreciate the opportunity to speak at events like this is because speeches are an important part of how the Federal Reserve delivers on its mission to the American people. Like my colleagues on the Federal Open Market Committee (FOMC), I enjoy engaging regularly with people from around the country to hear about on-the-ground economic conditions and to learn specifics about industries and communities. Such engagement is also a pathway to delivering better policy. It is important that households, businesses, and financial markets understand policymakers' views and assessments of economic conditions.

Monetary policy is transmitted to the rest of the economy through financial market prices, such as long-term interest rates, which in turn affect the decisions of households and businesses. Changes in the target range for the federal funds rate are transmitted to short-term interest rates through arbitrage relationships. Short-term interest rates and central bank communication, in turn, affect long-term interest rates through investors' expectations. According to the expectations theory of the term structure of interest rates, intermediate- and long-term interest rates are the weighted average of expected future short-term interest rates. In addition, monetary policy affects risk premiums. Tighter monetary policy tends to reduce the willingness of investors to bear risk, making them less willing to invest in long-term assets, which means that their return should be higher for investors to buy these assets.

Former Fed Chair Ben Bernanke nicely summarized how important central bank communication is for the transmission of monetary policy by saying that "monetary policy is 98 percent talk and only two percent action."2 While obviously hyperbole, the point is meaningful. Clear communication is an important part of a Fed policymaker's job.

Today the Fed communicates in a variety of ways, including policymaker speeches, Chair Powell's press conferences, and even through the Fed's social media channels. Clear and ample communication, however, has not always been the hallmark of the Fed. In the 1990s, cable news outlets would attempt to spot former Fed Chair Alan Greenspan walking into the building on the day of FOMC meetings. Commentators would pay careful attention to the size of his briefcase.3 The thought was that if the Chair was advocating a rate change, the briefcase would be bulging with documents to convince fellow policymakers. A light bag, on the contrary, would have signaled that a status quo policy decision was likely. Former Chair Greenspan seemed to value the element of surprise. In 1987, he famously quipped, "If I seem unduly clear to you, you must have misunderstood what I said."4 That said, during his tenure in later years, he initiated substantial changes in how Fed policymakers communicate with the public.

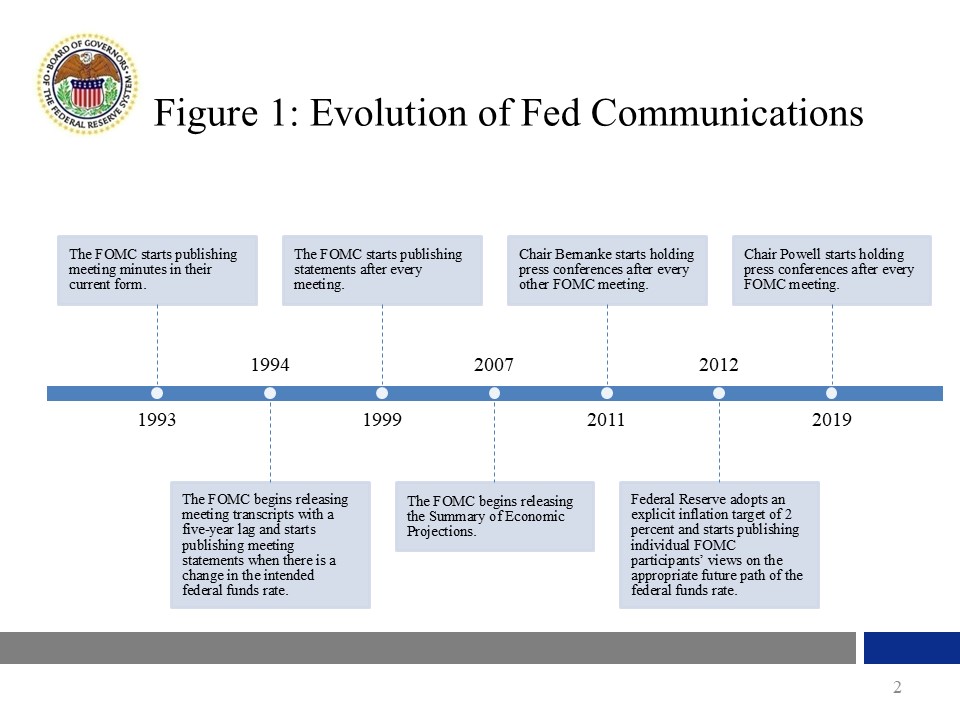

Figure 1 shows a timeline of the steps taken toward increasing transparency at the Fed since the 1990s. Beginning in 1993, the Fed started to publish FOMC meeting minutes in their current form at the next meeting. Soon after that, the Committee began releasing full transcripts of what was said at the meetings with a five-year lag. The next year, the FOMC started to issue statements following meetings at which there was a change in the policy stance. Before such public statements, Fed watchers would need to observe movements in markets to determine if a policy change was being implemented. In subsequent years, the target federal funds rate was incorporated into these statements, and then, in 1999, the FOMC started to publish statements after every meeting, regardless of whether there was a policy change. In 2004, the FOMC accelerated the release of the minutes to three weeks after the meeting. The Fed's transparency increased further under former Chair Bernanke. In November 2007, the FOMC began releasing the Summary of Economic Projections, commonly known as the SEP, which, as you may know, is a compilation of individual policymakers' forecasts for output, unemployment, and inflation. Since 2012, the SEP has also included information about policymakers' projections of appropriate monetary policy, known as the dot plot. Former Chair Bernanke started holding press conferences after every other FOMC meeting in 2011. In 2012, the FOMC published the Statement on Longer-Run Goals and Monetary Policy Strategy, which is known as the consensus statement. That statement articulates the FOMC's framework for the conduct of monetary policy in pursuit of the dual-mandate goals assigned by Congress: maximum employment and price stability. And since then, the FOMC has undertaken periodic public reviews of that statement. Under Chair Powell's tenure, starting in 2019, the Chair's press conferences have been held after every FOMC meeting.

Of course, the Chair and other policymakers also regularly testify before Congress, as required by law. And the Fed releases many reports and data, including the Monetary Policy Report, the Financial Stability Report, and the Supervision and Regulation Report. Policymakers' public appearances also help inform the public about the Fed's goals and its strategies to achieve those goals.

Communication is not just about talking; it is also about listening. Policymakers listen to the steady beat of economic data, and the Board and the Reserve Banks conduct numerous surveys of financial market participants, businesses, and families. Some of what we hear is summarized in the Beige Book, published eight times per year. I also listen to experts and the public at events like this and Fed Listens events, several of which are planned for later this year.

Today, it is widely accepted that clear communication contributes greatly to effective transmission of monetary policy, especially because clear communication can affect the expected path of interest rates and financial conditions more generally. Former Cleveland Fed President Loretta Mester studied this issue closely and discussed that when policymakers are clear about their policy goals, aspects of the economy that can and cannot be influenced by monetary policy, and the economic information that influences their forecasts and policy decisions, the public will have a better understanding of monetary policy.5 The public can then incorporate that information into their saving, borrowing, employment, and investment decisions.

Economic Outlook

So, in that spirit of making sure the public is well informed, I will now share with you my outlook for the U.S. economy. Over the past two years, significant progress has been made toward the Fed's dual-mandate goals of maximum employment and stable prices. Labor market conditions are solid, and inflation has come down, though it remains somewhat elevated relative to our 2 percent goal. While the economy is in a solid position, surveys of consumers and businesses show heightened uncertainty about the economic outlook. It remains to be seen what these surveys imply about future spending and investment and the direction of the economy more broadly.

Economic Activity

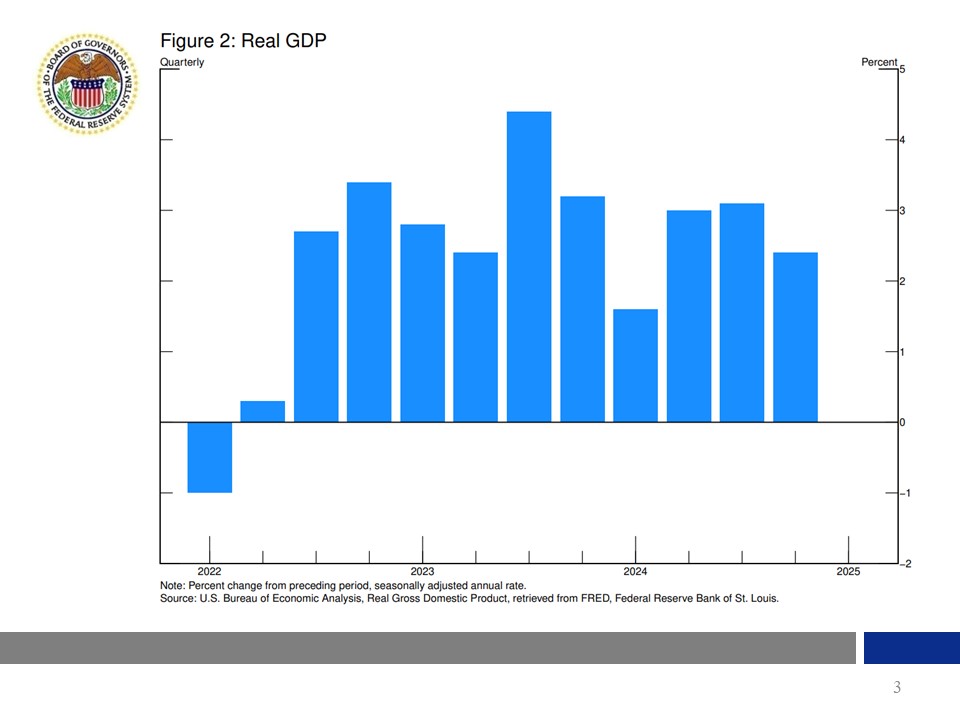

The economy expanded at a solid pace at the end of last year with gross domestic product (GDP) rising at a 2.4 percent annual rate in the fourth quarter, extending a period of steady growth, as you can see in figure 2. While Fed policymakers and many private-sector forecasters expect growth to continue, they broadly anticipate a slower pace of expansion this year. In the SEP released after the March FOMC meeting, the median participant projected GDP to rise 1.7 percent this year and to move up a bit below 2 percent over the next two years.

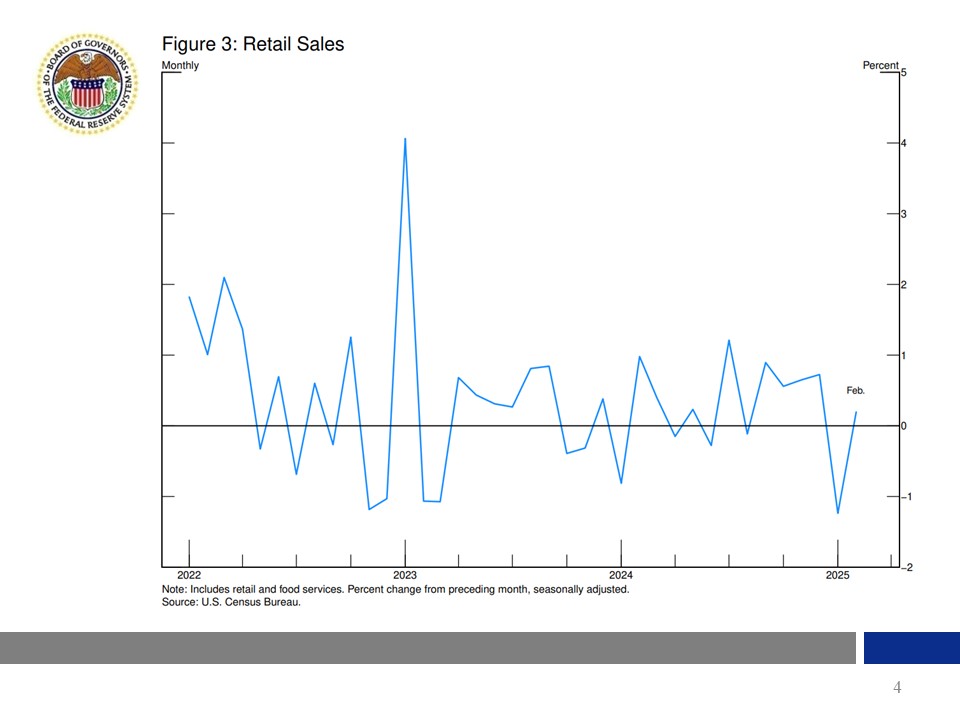

Resilient consumer spending has been the driving force of the current economic expansion. More recently, a few signs have emerged that suggest that some of the factors supporting last year's strong spending growth may be weakening. As you can see in figure 3, retail and food service sales rose 0.2 percent in February after falling a sharp 1.2 percent in January. That slower pace of spending could reflect seasonality, poor weather, and expected cooling after the strong spending at the end of last year. Nonetheless, the readings at the start of this year suggest less support for growth from household spending in the first quarter. The most recent Beige Book stated that contacts reported consumer spending was lower, on balance, with still solid demand for essential goods but increased price sensitivity for discretionary items, particularly among lower-income shoppers.6

Industrial production has increased for three straight months, including a 0.7 percent advance in February, which was led by a rise in manufacturing output, particularly motor vehicles. Like consumer sentiment, however, readings on business sentiment have also slipped. The Beige Book reported some increases in manufacturing activity, though it noted concerns raised by firms, including chemical products and office equipment makers, about the potential effect of changes to trade policy. Some manufacturing contacts in this region, the Sixth District, said that they expected demand to improve over the next 12 months but also noted risks around policy changes and global uncertainty.

If uncertainty persists or worsens, economic activity may be constrained. An important lesson learned in recent years, however, is that American consumers have been resilient, and negative sentiment reported in surveys often does not translate into a slowdown in actual activity.

Labor Market

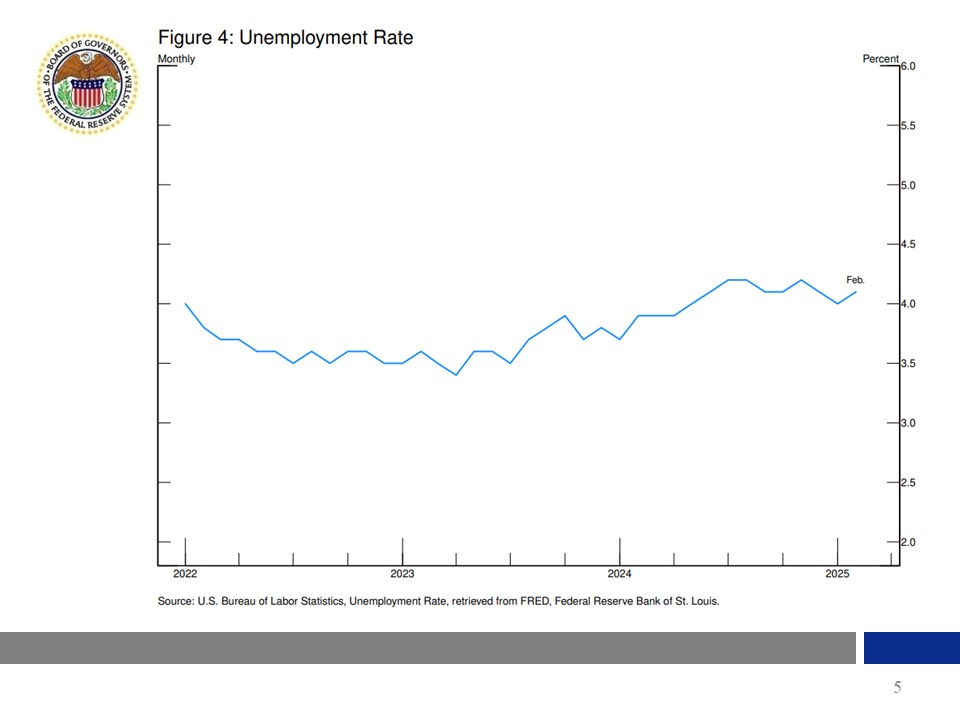

With respect to the labor market, conditions remain solid. The unemployment rate has remained low and was 4.1 percent in February. As you can see in figure 4, it has remained in a narrow range for the past year, consistent with broader evidence that labor market conditions have stabilized. That said, I anticipate that there could be some modest softening in the labor market this year. In the SEP projections, the median FOMC participant expected the unemployment rate to be 4.4 percent at the end of this year and 4.3 percent over the next two years.

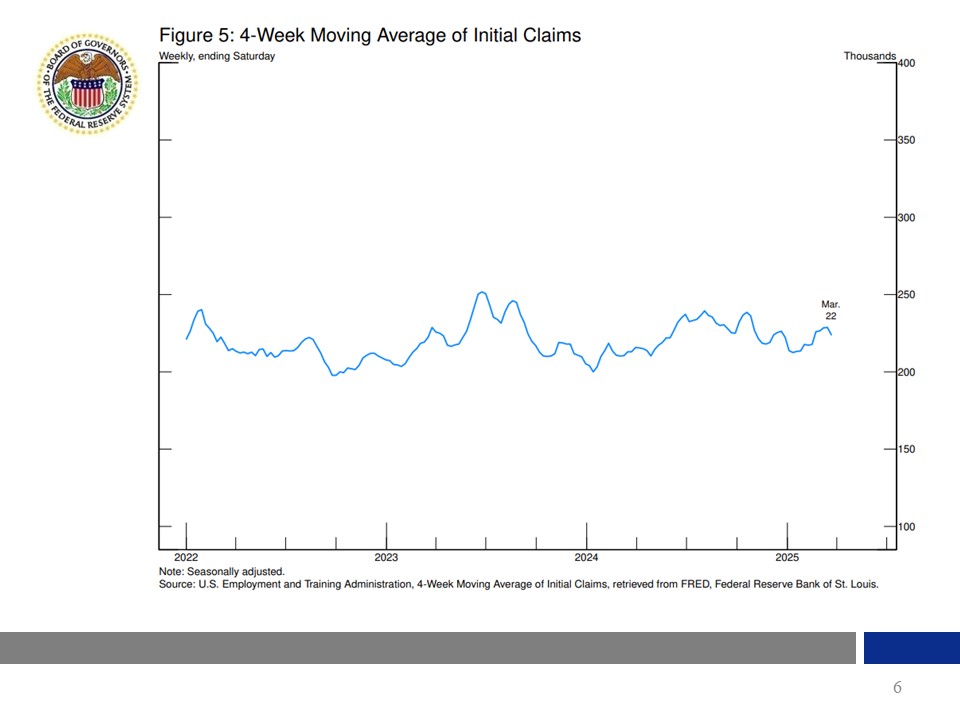

Payroll job gains have averaged nearly 200,000 per month over the past six months, through February. We will, of course, get additional data tomorrow with the March jobs report. The pace of job gains has cooled from its post-pandemic peak, but layoffs remain low. Figure 5 shows that new applications for unemployment benefits are largely holding steady this year and running at rates consistent with pre-pandemic levels. Low layoffs are a reason why the unemployment rate has been steady even as hiring has moderated. Recently, there has been an increase in former federal government employees seeking unemployment benefits and some uptick in claims filings in certain regions affected by those layoffs. I will be monitoring incoming data closely and remain vigilant about potential spillover effects in sectors such as education, health care, and state governments.

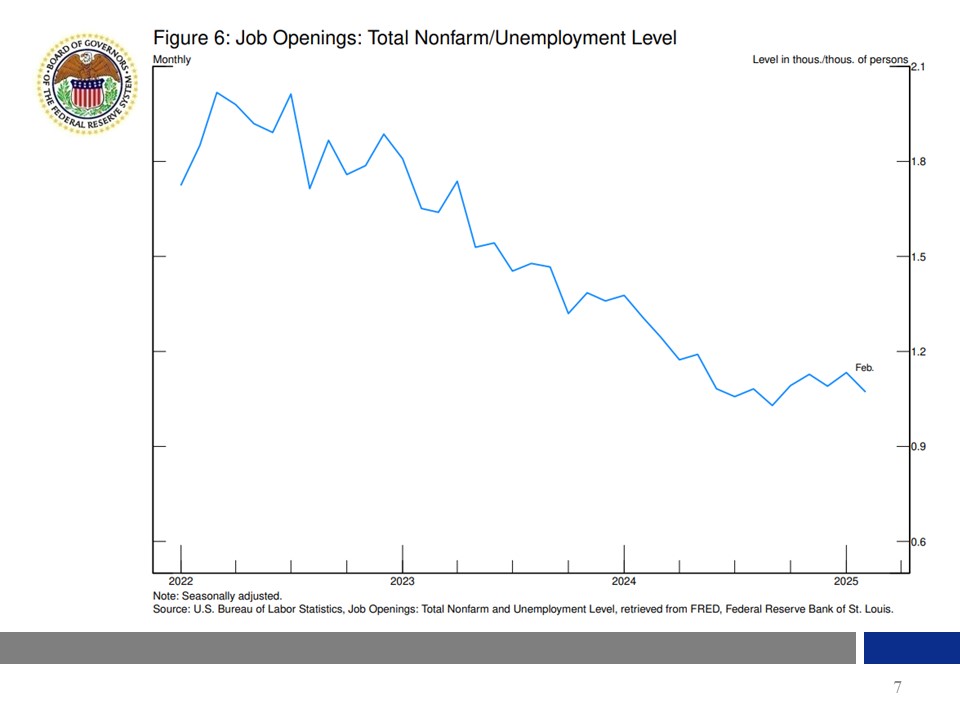

Looking at figure 6, you see that the gap between job openings and unemployed people seeking work has held steady for several months. That is another sign that the labor market is well-balanced. The gap has significantly narrowed from a peak in 2022, when the labor market was overheated. It is now consistent with 2019 readings, when the labor market was also solid and inflation low. Wages are growing faster than inflation and at a more sustainable pace than earlier in the pandemic recovery. The labor market is not a source of significant inflationary pressures.

Inflation

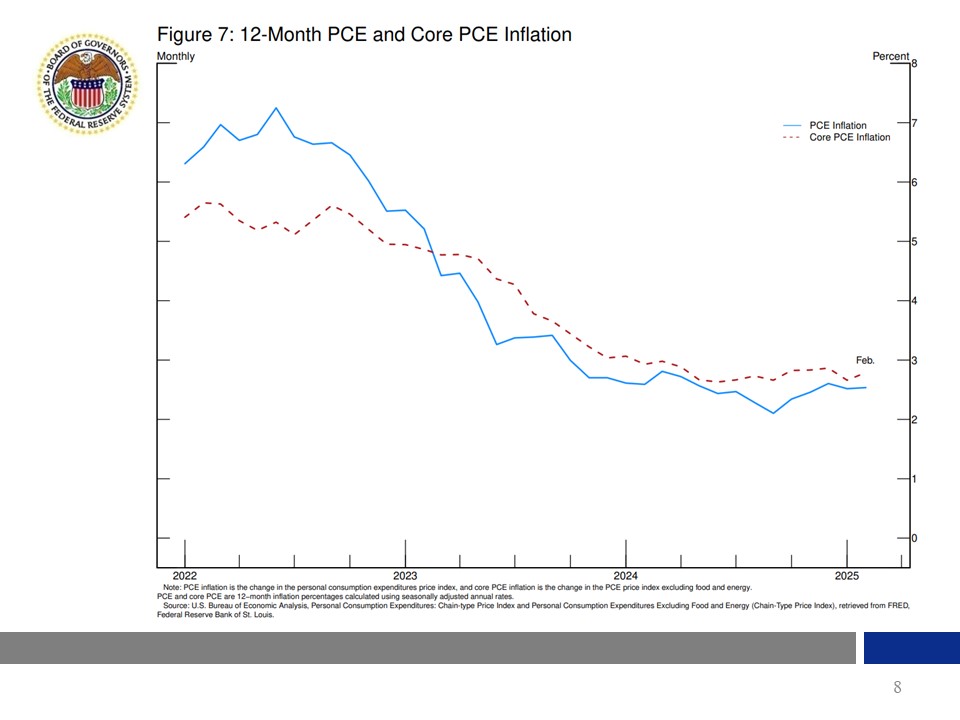

Inflation has come down a great deal over the past two and a half years but remains somewhat elevated relative to our 2 percent objective. Looking at inflation shown in figure 7, you see that the 12-month change in the personal consumption expenditures (PCE) price index peaked at 7.2 percent in June 2022. Since then, it has come down on an uneven path. In February, overall inflation was 2.5 percent on a 12-month basis. Core PCE inflation, which excludes volatile food and energy costs, shown by the dashed red line, peaked at 5.6 percent in 2022. In February, it was 2.8 percent.

While inflation is well down from its recent peak, the latest data have largely shown it moving sideways. The median FOMC participant forecasts overall PCE inflation at 2.7 percent this year and 2.2 percent next year. In 2027, the median projection is at our 2 percent objective. The prospect of tariffs has consumers and businesses reporting that they expect higher inflation in the near term. Beyond the next year or so, however, most measures of longer-term inflation expectations remain consistent with our 2 percent inflation goal.

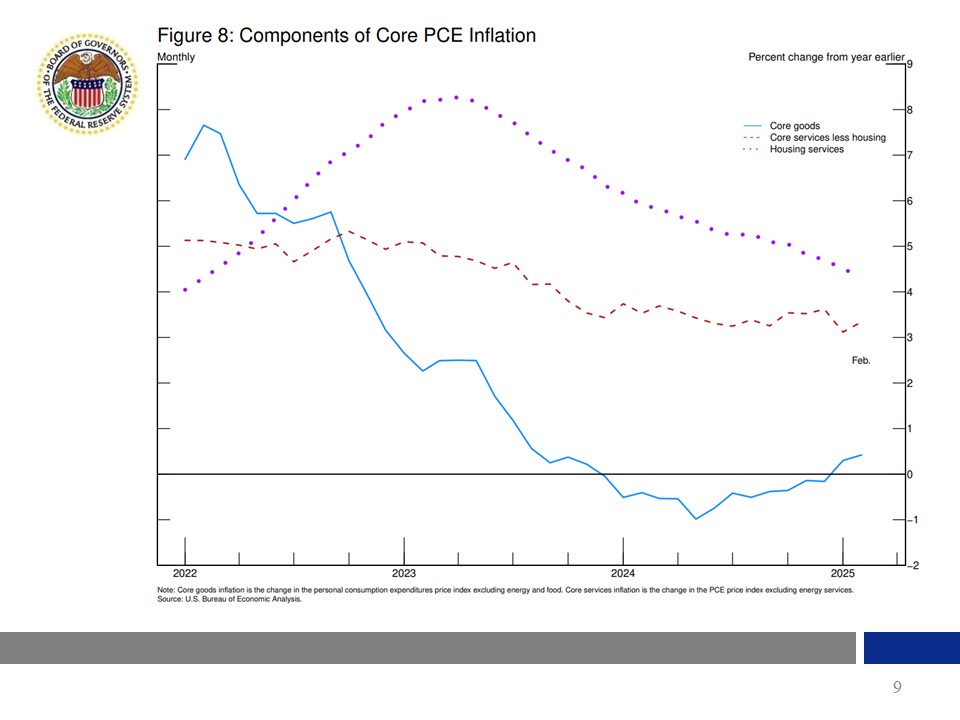

To better understand what is driving inflation, I think it can be helpful to look at some major components of changes in prices, as you can see in figure 8. Outside of food and energy, goods inflation was negative last year, helping to support overall disinflation. In more recent months, goods inflation has turned positive. That may in part reflect trade policy or the anticipation of changes to trade policy, but capturing the exact cause is difficult. Services inflation excluding housing, the dashed red line, has moderated from its peak but remains elevated. Housing services inflation, the dotted purple line, continues to move lower. If that trend continues, it could counter somewhat stronger inflation in other categories.

Monetary Policy

In the current environment, I attach a higher degree of uncertainty to my projections than usual. The most recent SEP indicated that other FOMC participants also were quite uncertain about the outlook: A greater number of participants indicated that uncertainty around their projections of GDP growth, the unemployment rate, and inflation was higher than average over the past 20 years compared with responses from the previous SEP round in December 2024. As I mentioned, consumer and business surveys show that much of the economic uncertainty they report is tied to recent developments in trade policy. Significant changes in trade, immigration, fiscal, and regulatory policies currently are in process. It will be crucial to evaluate the cumulative effect of these policy changes as we assess the economy and consider the path of monetary policy. Of course, at the Fed, we look at the whole of the economy and many factors that shape it.

I supported the FOMC's decision to hold rates steady at our last policy meeting in March. Growth has remained solid so far but has started to show some signs of slowing. Labor market conditions have remained stable through February, and progress on inflation has eased, but the outlook is uncertain. These conditions led me to favor holding the policy rate constant at what I view as a moderately restrictive level.

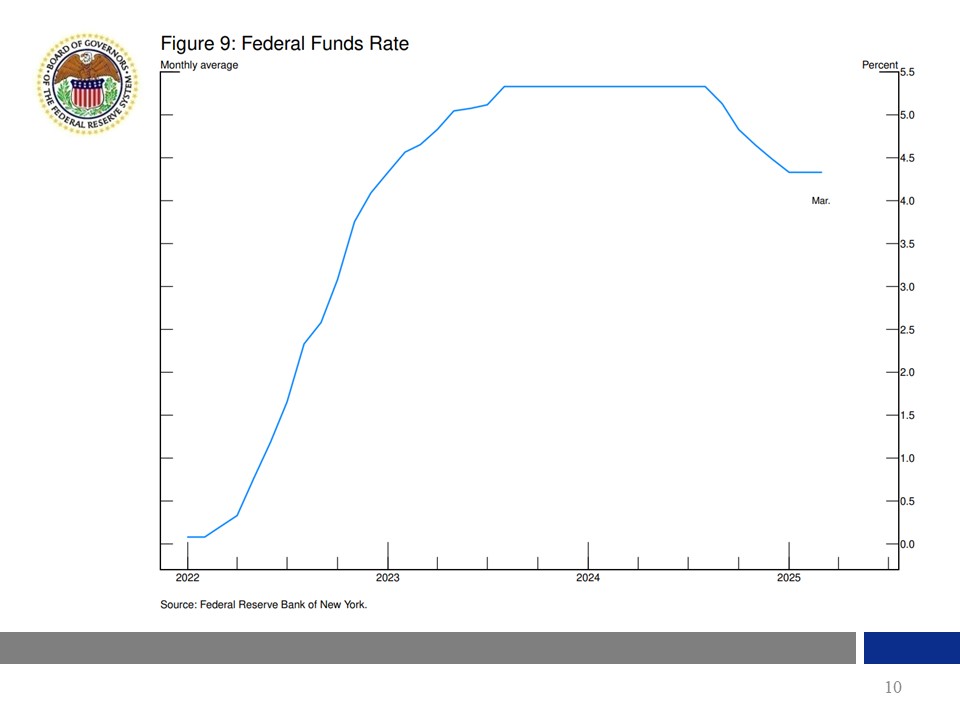

The longer-term perspective provided by figure 9 shows that the FOMC responded to elevated inflation in the post-pandemic period by raising the policy rate 5-1/4 percentage points over about 15 months, starting in March 2022. After the Committee held the rate at that restrictive level for more than a year, progress on inflation allowed it to lower its policy rate by 1 full percentage point last year to its current level. The outcome of inflation moderating toward the 2 percent target without a large increase in unemployment was historically unusual but greatly welcomed.

Thinking about the future path of policy, I will continue to assess incoming data, the evolving outlook, and the balance of risks. As we emphasize, monetary policy is not on a preset course. If the economy remains strong and inflation does not continue to move sustainably toward 2 percent, the current policy restraint could be retained for longer. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, policy could be eased accordingly. In my view, there is no need to be in a hurry to make further policy rate adjustments. The current policy stance is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.

Having provided you with my current economic outlook, I would like to conclude by circling back to where I started, with the value of central bank communication. The remainder of today's conference will touch on FOMC communications and monetary transmission, among other topics. In that sense, the remarks that I've just given may become tomorrow's data point! I appreciate the pursuit of research like that presented today, which helps us gain further insight into a wide range of topics relevant to monetary policymaking.

Thank you for your time today. I wish you a productive and informative remainder of the conference.

1. The views expressed here are my own and are not necessarily those of my colleagues on the Federal Reserve Board or the Federal Open Market Committee.

2. See Ben S. Bernanke (2015), "Inaugurating a New Blog," Ben Bernanke's Blog, March 30, paragraph 1.

3. See William T., Gavin and Rachel J. Mandal (2000), "Inside the Briefcase: The Art of Predicting the Federal Reserve," Federal Reserve Bank of St. Louis, Regional Economist, July 1.

4. See Binyamin Appelbaum (2012), "A Fed Focused on the Value of Clarity," New York Times, December 13.

5. See Loretta J. Mester (2018), "The Federal Reserve and Monetary Policy Communications," speech delivered at the Tangri Lecture at Rutgers University, New Brunswick, New Jersey, January 17.

6. See Board of Governors of the Federal Reserve System (2025), The Beige Book: Summary of Commentary on Current Economic Conditions by Federal Reserve District (PDF), February.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}