I am happy to have the opportunity to return to and to speak in Dakar. Not far from here, I began my unexpected journey into the economics profession.1 As a graduate student at l'Université Cheikh Anta Diop de Dakar, I came to study philosophy and to write a thesis in African philosophy. However, I immediately started posing questions that became foundational in my conversion to economics, which would help provide the framework and skills to respond to these questions. Among them were the following: Why did a ballpoint pen that cost $0.10, at that time, in the United States cost the equivalent of $10 in Senegal? Why were some countries rich and some poor? Is there ultimately convergence among economies and one path to economic development and higher standards of living? Questions like these ignited my interest in understanding how the economy and monetary policy affect people's lives.

I have been lucky enough to return to Africa many times. That included working in Rwanda and East Africa in the late 1990s and early 2000s, where M-Pesa, a mobile phone–based money transfer service, and other innovations piqued my interest in technologies that facilitate faster movement of capital and payments. I feel very fortunate to return to Dakar today, after many years, and to engage with an issue that is having a notable effect on the global financial system: tokenization in financial markets. Tokenization could specifically offer compelling benefits in West Africa and other emerging economies, including potentially faster cross-border payments and better access to capital markets.2

More broadly, tokenization could facilitate improvements upon frictions in financial markets today, with purported benefits ranging from improvements in settlement times, as well as enhanced recordkeeping and automation, to new ways of using traditional assets. This potential warrants careful consideration of the innovation's opportunities and challenges, particularly from a central bank perspective. If you will indulge me, three dimensions of tokenization will be my focus today: I will more deeply explore (1) the opportunities tokenization could provide, (2) financial-stability considerations and potential challenges should the innovation scale, and (3) the Fed's role with respect to tokenization and digital assets more broadly.

Before diving in, I want to highlight two grounding principles. First, I support and encourage financial innovation. Second, I carefully monitor the financial-stability implications that accompany all innovation. It is my responsibility as a monetary policymaker to know and weigh these opportunities and risks. This responsibility applies to my role at the Federal Reserve, where I serve as the chair of the Board's Committee on Financial Stability, and in my roles with the Financial Stability Board (FSB). I am both co-chair of the FSB's Regional Consultative Group for the Americas and a participant on the Standing Committee on Assessment of Vulnerabilities. These roles allow me to apply a financial-stability lens to issues that could affect the financial system at a global level.

Tokenization in the Context of Financial Markets

To start, allow me to define tokenization for our purposes today. The term "tokenization" is broad and takes on different meanings in different contexts. In the broadest sense, tokenization refers to the concept of representing any number of items digitally. The concept has been applied to fine art, music royalties, and even soccer cleats.3 In the context of financial market innovation, tokenization is generally thought of as the process of generating and recording a digital representation—a token—of an asset on a new platform or technology, such as distributed ledger technology (DLT).4 Blockchain is a common form of DLT in which details of transactions are recorded in blocks of information.5 Generally, an asset is considered "tokenized" when a DLT is used to record ownership of that asset. Transactions involving tokens are then constructed using "smart contracts," or computer code that can execute predefined actions once certain conditions are met, among other capabilities. Many of the potential benefits of tokenization flow from this automated and programmable functionality.

This relatively new innovation is already showing promise, potentially deepening connections between innovative technologies and traditional financial systems. Financial markets may be primed to adopt this technology for two reasons. First, they benefit from established liquidity, infrastructure, and regulatory frameworks that can be leveraged; second, they contain siloed systems and processes that involve multiple intermediaries and manual steps that are, in many cases, amenable to enhancements from the automation and programmability offered by tokenization. It is this intersection between large existing markets—such as bonds, money market fund (MMF) shares, and repurchase agreements (repos)—and opportunities for new functionality or efficiencies in areas such as collateral and liquidity management that could drive the adoption of tokenization in financial markets.

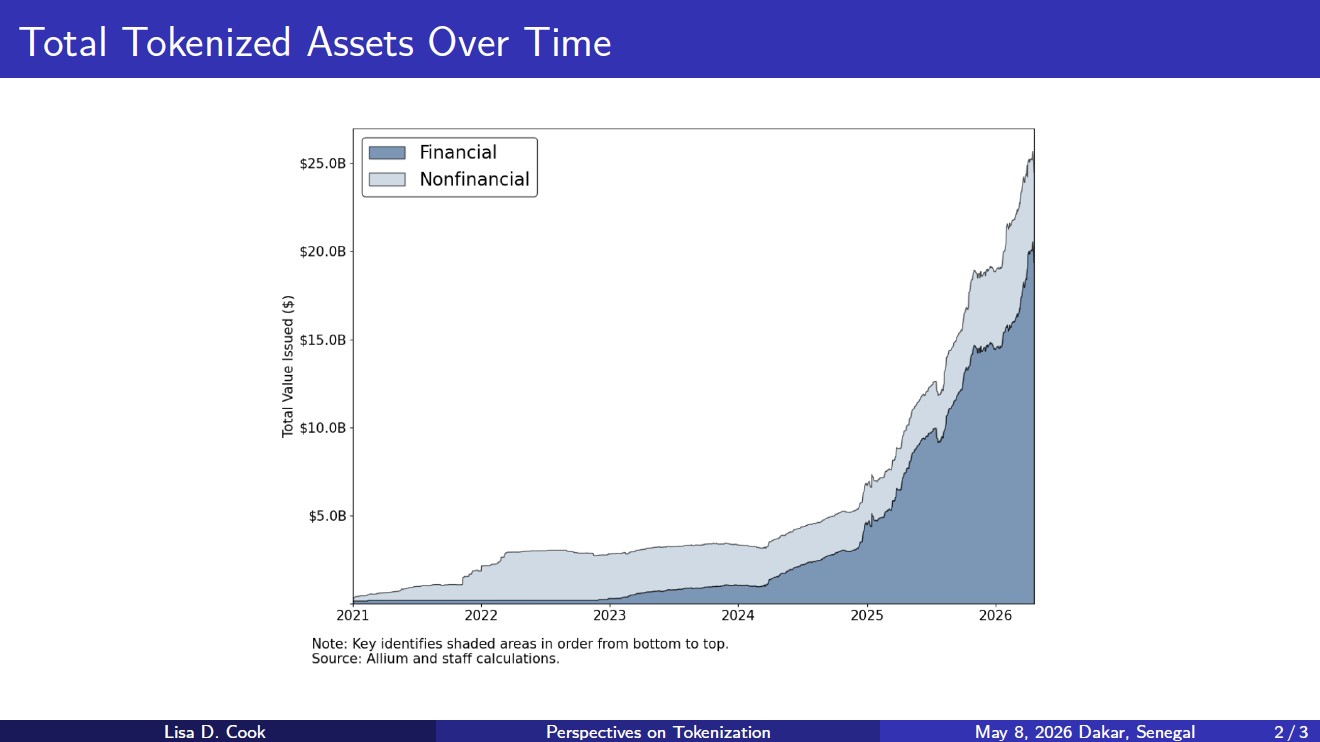

We already observe increased interest and investment in tokenization in financial markets, with tokenized assets in the U.S. more than doubling their market capitalization in the last year to around $25 billion.6 Let's take a closer look at some of the trends over time. Figure 1 shows growth over the past five years, separating financial assets (in dark blue) from nonfinancial assets (in light blue). This growth is being driven in part by the entrance of large financial institutions into the market, often in collaboration with emerging fintech firms with expertise in blockchain technology.

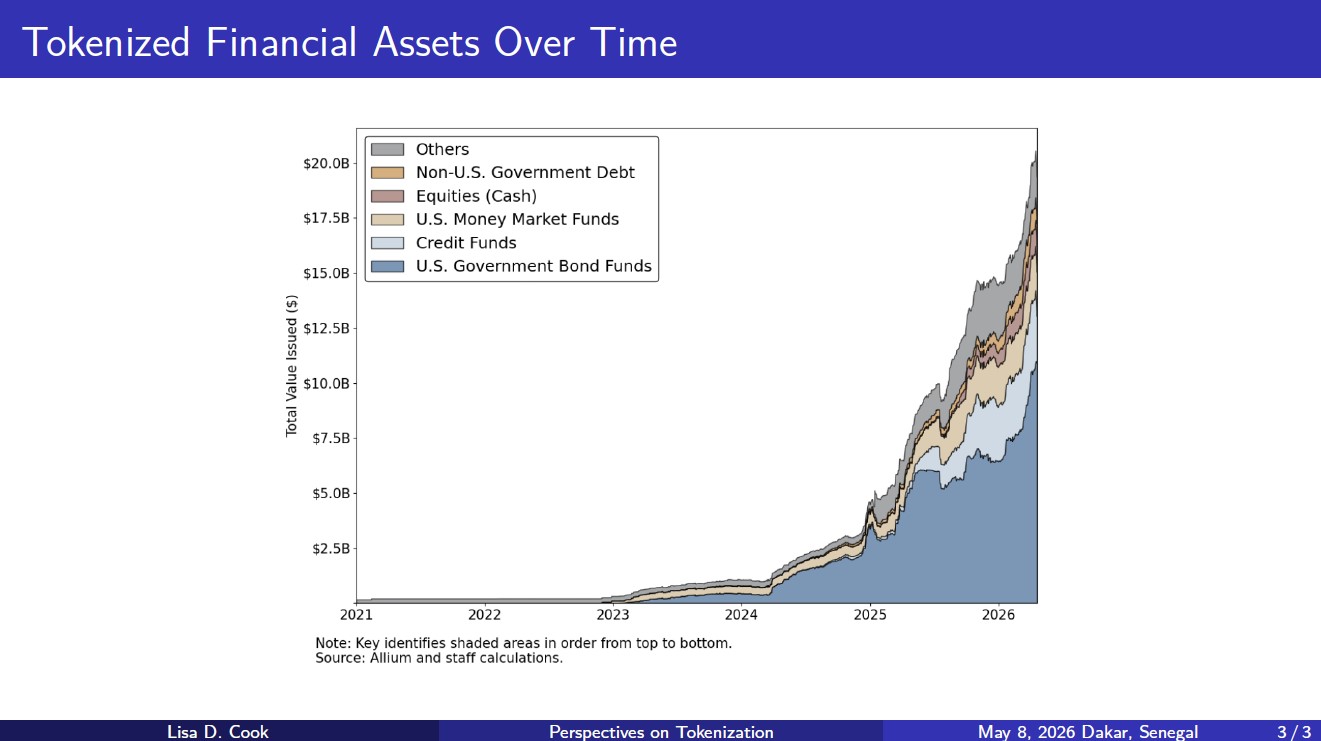

Figure 2 takes a closer look at the recent growth in tokenized financial assets. The largest category is government bond funds (in dark blue). Meanwhile, credit funds (in light blue) and MMFs (in beige) are growing quickly. While still small relative to the size of the asset classes being tokenized, this growth represents increasing interest in leveraging this technology for facilitating wholesale transactions, earning on-chain interest income, and enabling broader cross-border ownership.

Tokenization Framework

With this context in mind, I would like to briefly walk through a framework for thinking about different forms of tokenization. I think of innovations in tokenization along two dimensions: (1) the infrastructure, or rails, that assets are transferred on and (2) the assets themselves.

In terms of infrastructure, tokenization involves new platforms and arrangements utilizing DLT, including blockchains, that can provide new features and functionality for financial market transactions. Those features include programmability through smart contracts, or executing transactions when certain predefined conditions are met, and composability, or creating products that combine features and functions in new ways.7 For example, smart contracts can enable multiple legs of a transaction to be combined and executed automatically, such as the settlement of two linked foreign exchange transactions. Such features could support the construction of complex trades and enable the execution of financial transactions in more flexible and efficient ways.

In terms of the assets themselves, I see them as taking two primary forms. One is directly issued assets. In this case, assets are issued and custodied directly on DLT without an underlying conventional reference asset. Therefore, the actual issuance and transfer of ownership occur entirely on blockchain rails. Financial instruments issued solely on DLT could include a variety of claims on the issuer, such as bonds or other debt instruments, although such products are currently rare.

The other form is representations of assets that were originally issued via conventional means. In this form, the reference assets are locked and remain in the existing legacy markets and clearing systems, but ownership is represented via tokens on a blockchain. This type of tokenization could allow a token holder to have a legally enforceable ownership claim over the token's reference asset, such as government bonds, corporate equity, MMFs, or a nonfinancial asset like a barrel of oil or a warehouse. The remainder of my remarks will focus on this form of tokenization. As you can see, the possibilities for new kinds of financial arrangements with tokenization are very broad, and this type of framework helps assess potential opportunities and challenges presented by the technology.

Opportunities and Benefits

Having established that this is a fast-growing field filled with notable recent innovations, allow me to take a deeper dive into potential opportunities related to tokenization in financial markets. I can understand why financial firms are exploring this technology, as it demonstrates the potential to enhance transparency, improve efficiency through automation, and offer settlement flexibility in financial market transactions. Many of these benefits are illustrated through improvements to collateral mobility and liquidity management processes, which I view as the major use case for financial institutions. More broadly, tokenization could also increase competition and expand market access to different assets. Let me expand on each of these opportunities.

First, tokenization could improve existing collateral and liquidity management processes in several meaningful ways. Current operational workflows for collateral and repo markets can include manual and fragmented processes that require reconciling data pools across disparate legacy systems. This can lead to delays, errors, and additional costs. Tokenization could allow recordkeeping to be streamlined through solutions that allow parties to share a single transparent source for tracking transactions and managing associated collateral. In addition, smart contracts can automate complex activities that currently require manual intervention, such as margin calls and collateral substitutions, increasing operational efficiency. Moreover, using tokenized funds to meet margin requirements can simplify investors' cash management and dampen redemption pressure, thus mitigating possible stress events in funding markets and improving financial stability.8

Perhaps most significantly, tokenization and programmable contractual terms enable new types of transactions to occur intraday for capital and liquidity management. For example, tokenized MMFs enable frequent intraday investment and redemption, enhancing returns on idle cash. In addition, programmable contracts enable tokenized repo transactions to occur intraday, providing more timely access to liquidity than current overnight processes. This has recently become a significant institutional use case.9

Another aspect is the technology's versatility, which allows it to support complex multicurrency and multi-asset transactions. Tokenization could facilitate settlement across multi-leg transactions and reduce the time gap between trading and settlement, which, under current practices, often takes an additional business day to settle post-trade and relies on traditional operating hours. Additionally, programmability allows tokens to function across trading, lending, and collateral applications, increasing flexibility in how assets can be used. For example, a repo combined with a foreign exchange transaction would seem highly relevant for countries within the Central Bank of West African States (BCEAO) and for neighboring countries or those trading with BCEAO countries. Since repos represent a major source of funding and liquidity management for large financial institutions, even marginal efficiency gains could translate into significant cost savings for market participants.

In terms of broader market dynamics, tokenization can foster competition and new forms of market collaboration. Tokenization can potentially lower operational barriers to entry for emerging financial services firms to compete with traditional institutions. We are seeing this activity already in the market, with existing institutions, including major exchanges, partnering with these new firms to enable more efficient development of new products and services.10

Finally, tokenization could expand market access in a way that is beneficial to both individuals and institutions. One of the benefits of the technology is the ability to use assets in new or more flexible ways. Programmable fractional ownership, for example, could allow for more flexible and expanded opportunities for investors by enabling small-denomination exposure with more flexible and automated transfer of ownership. The capabilities related to fractional ownership may be especially attractive in developing economies, including those in West Africa, where savers and investors may have fewer resources to invest but where a need exists to bolster capital markets as a complement to the social safety net. (Of course, I would simultaneously advocate for appropriate investor protections.)

To be clear, I do not see tokenization as replacing traditional market infrastructure. And it is important to acknowledge that certain barriers are in place in existing systems for policy or prudent risk-management purposes. Rather, the integration of these emerging capabilities with traditional infrastructures and established legal frameworks offers the opportunity to improve the efficiency and function of the entire financial system.

Financial Stability Considerations

While I am optimistic about the possibilities, I am also cognizant of the financial-stability considerations that must be monitored should tokenization scale. At its core, tokenization in financial markets requires the management of the same types of risks we have in markets today. However, it is important to consider how risk dynamics could change or manifest in new or different ways with this technology. From my perspective as a policymaker, understanding these dynamics will both support financial stability and enable innovations to scale safely. I am monitoring closely a broad range of potential vulnerabilities, but I want to focus on two considerations most relevant to developments in financial markets: liquidity implications and interconnectedness.

First, consider liquidity transformation in the financial system. Some tokenized assets can be redeemed on demand and at par with the issuer, who typically invests in a pool of less liquid assets, thereby introducing run risk. Tokenization might change the incentives of investors to redeem their assets with the issuer, which, in turn, could entail benefits for or risks to financial stability. The ability to use the tokenized assets instead of cash to pay for transactions or meet margin calls might reduce the need to redeem them to obtain liquidity and, consequently, alleviate the need for the issuer to sell assets to meet redemptions. Another potential benefit is the ability to source liquidity if secondary markets for tokenized assets develop, which might be especially valuable for institutions that perform maturity transformation. On the risk side, tokenization enhances the issuer's exposure to shocks in secondary markets that could be unrelated to the underlying reserve assets or solvency concerns about the issuer.11

Related to liquidity considerations, the 24/7 nature of trading and settlement on public blockchains may facilitate market participants gaining access to intraday liquidity sources, which can be particularly valuable in times of stress, as those participants may need to post collateral with counterparties outside of the trading day or with central bank liquidity facilities. As to risks, around-the-clock trading and settlement may speed up a run on the issuer if disruptions in the market for tokens outside normal market hours escalate.

Second, consider the nexus between tokenized assets and traditional markets. The use of tokenized assets as collateral, as an instrument to access liquidity, and as a reserve asset expands the channels of shock transmissions within the digital asset ecosystem and to the traditional financial system. Likewise, interconnections between issuers of tokenized assets and other entities in the form of cross holdings of their liabilities might create problems in the event that an issuer liquidates assets that are liabilities of another issuer. Relatedly, because the reserve assets of some issuers are held in the traditional financial sector, the digital asset ecosystem might amplify shocks at the same time they are transmitted to the traditional financial system. As a benefit, firms may take advantage of the convenience associated with tokenized assets to obtain funding through markets for digital assets, possibly enhancing their ability to diversify their sources of funding or to collateralize their loans in the traditional financial market by appealing to a broader investor base.

As I previously mentioned, tokenization could also allow for new varieties of complex, interrelated transactions as conventional assets are used in new ways. However, tokenizing conventionally issued assets still fundamentally relies on connections to and communication with existing financial infrastructure, which may not operate every hour of every day. Relatedly, opaque or illiquid assets create a potential disconnect between token liquidity and underlying asset liquidity. These interconnections could introduce additional complexity and dependencies in the financial system.

And, as with any new technology, one must also consider operational fragilities and security concerns. As processes become more automated, such as with smart contracts, humans are less able to correct for bugs or respond to outside threats. In addition, relatively new products and systems tend to be targeted by malicious actors looking for exploitable vulnerabilities, and cyberattacks are relatively common in the DeFi ecosystem.12

I highlight these considerations because fully assessing and understanding tradeoffs between opportunities and risks is how we enable innovations to scale safely and sustainably. Ultimately, the Fed's efforts to maintain financial stability are a service to the American people, and I know my global peers take a similar mindset.

Conclusion

As a Fed policymaker, I see my role as supporting responsible innovation while being clear-minded about both the opportunities and challenges innovations, including tokenization, present to the global financial system. As many in this room know, the Fed is engaging with other organizations and global peers to both monitor and support responsible innovation. This work reflects the interconnectedness of the global financial system and includes collaboration with multilateral institutions, such as the Bank for International Settlements and the FSB, bilateral engagements with peer central banks, and ongoing dialogue with the industry to monitor, analyze, and better understand these developments. And, within the Federal Reserve Board, we are researching and experimenting to fully understand tokenization and its implications.13

To conclude, I applaud and encourage innovation in the financial system. Tokenization in financial markets is growing rapidly, which warrants a closer understanding of its potential. While I do not see tokenization as substituting for traditional market infrastructure, the technology presents a tremendous opportunity for innovation in the sector. I see that from my seat in Washington and understand how those opportunities could be as great or greater here in West Africa. At the same time, I am mindful of financial stability considerations. At the Fed, we vigilantly monitor an ever-shifting landscape of vulnerabilities, and I know my peers around the globe are doing the same. With fast-moving innovations, it is incumbent that we take the time to understand them. Events like this energize learning and make those critical discussions possible. I am honored to be asked to speak here today. It is beyond humbling to return to Dakar as a Federal Reserve Governor because this is the very place that catalyzed the career journey that led me to this role.

Thank you once again.

1. The views expressed here are my own and are not necessarily those of my colleagues on the Federal Reserve Board or the Federal Open Market Committee.

2. See Tobias Adrian (2026), "Tokenized Finance (PDF)," IMF Notes Series 2026-001 (Washington: International Monetary Fund, April).

3. For example, see Taylor Ryker (2025), "The Tokenization of Fine Art: A Revolutionizing Investment in a Traditionally Exclusive Asset Class," CoolWave Capital, May 19, https://medium.com/@coolwavecapital/the-tokenization-of-fine-art-a-revolutionizing-investment-in-a-traditionally-exclusive-asset-class-653cd7e8f24b; Mike Butcher (2023), "Success with Rihanna's Music Rights Helps Web3 Marketplace Raise Fresh VC Round," TechCrunch, May 16, https://techcrunch.com/2023/05/16/success-with-rihannas-music-rights-helps-web3-marketplace-raise-fresh-vc-round; and Ana Yglesias (2024), "Lionel Messi Releases Replica Cleat Collectible with RWA Tokenization Platform Planet," Yahoo, March 6, https://www.yahoo.com/lifestyle/lionel-messi-releases-replica-cleat-175045113.html.

4. See Bank for International Settlements and Committee on Payments and Market Infrastructures (2024), Tokenisation in the Context of Money and Other Assets: Concepts and Implications for Central Banks (PDF) (Basel: BIS and CPMI, October). These remarks focus on tokenized financial assets rather than tokenized forms of money and payment instruments.

5. See Financial Stability Board (2023), The Financial Stability Risks of Decentralised Finance (PDF) (Basel: FSB, February).

6. This was calculated by staff using data from Allium Labs.

7. See Financial Stability Board (2024), The Financial Stability Implications of Tokenisation (PDF) (Basel: FSB, October).

8. In March 2020, for example, MMF investors partly met margin calls in repo and derivatives contracts by redeeming their MMF shares, amplifying stress and instability in funding markets. In contrast, the ability to post tokenized shares for margin requirements could mitigate such stress, as those tokenized funds are considered the same as cash for margin purposes, and thus would not need to be sold. Only in the event of default might those margins need to be liquidated to close the position they secure. For more details, see Pablo Azar, Francesca Carapella, JP Perez-Sangimino, Nathan Swem, and Alexandros P. Vardoulakis (2025), "The Financial Stability Implications of Tokenized Investment Funds," Federal Reserve Bank of New York, Liberty Street Economics (blog), September 24.

9. For example, one market participant recently announced processing over $400 billion in daily repo transactions on its tokenized settlement platform; see Broadridge (2026), "Broadridge's Distributed Ledger Repo Achieves 392% Year over Year Growth; Processes $8 Trillion in March," news release, April 9, https://www.broadridge-ir.com/news/news-details/2026/Broadridges-Distributed-Ledger-Repo-Achieves-392-Year-Over-Year-Growth-Processes-8-Trillion-in-March/default.aspx.

10. For example, see Vicky Ge Huang (2026), "NYSE Partners with Securitize to Develop 24/7 Tokenized Securities Platform," Wall Street Journal, March 24, https://www.wsj.com/finance/stocks/nyse-partners-with-securitize-to-develop-24-7-tokenized-securities-platform-871a4c7e; and Vicky Ge Huang (2026), "Nasdaq Partners with Kraken in Plan for 24/7 Tokenized Stock Trading," Wall Street Journal, March 10, https://www.wsj.com/finance/stocks/nasdaq-partners-with-kraken-in-tokenization-push-135e8112?mod=article_inline.

11. For more details, see Azar and others, "The Financial Stability Implications of Tokenized Investment Funds" (note 8).

12. See, for example, Laurence Bristow and Marco Macchiavelli (2026), "Crypto Hacks and DeFi Runs," Bank Policy Institute, April 23, https://bpi.com/crypto-hacks-and-defi-runs.

13. See, for example, Francesca Carapella, Grace Chuan, Jacob Gerszten, Chelsea Hunter, and Nathan Swem (2023), "Tokenization: Overview and Financial Stability Implications," Finance and Economics Discussion Series 2023-060r1 (Washington: Board of Governors of the Federal Reserve System, September; revised December 2023); Azar and others, "The Financial Stability Implications of Tokenized Investment Funds" (note 8); Kenechukwu Anadu, Patrick McCabe, JP Perez-Sangimino, and Nathan Swem (2026), "A Framework for Understanding the Vulnerabilities of New Money-Like Products," Finance and Economics Discussion Series 2026-002 (Washington: Board of Governors of the Federal Reserve System, January); and Cy Watsky, Matthew Liu, Nolan Ly, Kurtis Orr, Amber Seira, Zach Vida, and Lawrence Wu (2024), "Tokenized Assets on Public Blockchains: How Transparent Is the Blockchain?" FEDS Notes (Washington: Board of Governors of the Federal Reserve System, April 3).

{kind=link}

{kind=link}