Policy Statement Concerning Mandatory Arbitration

The second item on today’s agenda is a recommendation that the Commission issue a policy statement[1] (the “Policy Statement”) addressing the presence of a mandatory arbitration provision in the governance documents of a company registering offers and sales of securities and its impact on the acceleration of the effectiveness of the registration statement. In this context, a mandatory arbitration provision requires an investor to arbitrate its claims arising under the federal securities laws with the issuer of the securities.

There are two separate questions with respect to mandatory arbitration. First, what is the state of the law on the permissibility of mandatory arbitration provisions? Second, assuming such provisions are allowed, should a company adopt mandatory arbitration?

The answer to the first question sits at the intersection of the federal securities laws, state corporate law, and the Federal Arbitration Act of 1925 (the “Arbitration Act”). The expertise and domain of the Commission and its staff is, of course, in the federal securities laws. Accordingly, the Policy Statement provides the Commission’s views on whether mandatory arbitration provisions are inconsistent with the federal securities laws – and concludes that they are not.

While I am pleased that the Commission is voting today on whether to issue the Policy Statement, I must note that the agency is, unfortunately, at least a decade too late in taking this action. Over the past forty years, federal courts, including the Supreme Court, have issued several decisions informing the analysis of whether the federal securities statutes override the Arbitration Act. As the Policy Statement details – and the staff’s presentation will highlight – the law in this area has been clear since at least 2013.[2]

Despite the abundant judicial decisions on this issue, the Commission has not publicly shared its views on this topic since an amicus brief it submitted in 1986.[3] The agency has, however, scrutinized registration statements filed by companies that have sought to include a mandatory arbitration provision in their governance documents – and injected uncertainty into whether these registration statements would be declared effective.[4] Companies contemplating an IPO today may interpret these prior actions to reflect the Commission’s current views on the issue. As an agency that trumpets the importance of disclosure and transparency, the Commission’s lack of a recent public position on this important topic is unmoored from both its mission and its mandate. However, that ends today if the Commission approves the Policy Statement.

Of course, when analyzing whether mandatory arbitration provisions are valid, companies must also consider state corporate law. This issue has become more crucial in light of Delaware’s recent amendments, which became effective just last month, to its General Corporation Law that may prohibit a company’s governance documents from including a mandatory arbitration provision.[5] Other states may take different approaches. Neither the Commission nor its staff has the expertise to address a provision’s enforceability under state law and any preemption concerns raised by the Arbitration Act with respect to state law. Regardless of the validity of mandatory arbitration under state corporate law, the Policy Statement provides companies with the clarity that the presence of a mandatory arbitration provision will not impact decisions regarding whether to accelerate the effectiveness of a registration statement.

Turning to the second question – with clarity under the federal securities laws and assuming validity under state corporate law – should a company adopt a mandatory arbitration provision? I expect there to be robust public debate on this issue among various interested parties. I have views on this issue, and I am sure that my fellow Commissioners do as well. However, the Commission, as a body, will not be part of this debate because it is outside of the scope of the matters over which the Commission has authority under the federal securities laws.

The Commission’s statutory criteria in deciding whether to accelerate the effectiveness of a registration statement is to ensure complete and adequate disclosure of material information to the public.[6] In other words, the Commission is not a merit regulator that decides whether a company’s particular method of resolving disputes with its shareholders is “good” or “bad.” Consistent with this directive, the Commission should not participate in a debate on whether mandatory arbitration provisions are “good” or bad” for companies and their shareholders. Rather, the Commission and its staff should focus on ensuring complete and adequate disclosure of material information concerning a company’s mandatory arbitration provision, if one exists. This approach is in keeping with how the agency has treated certain other provisions that companies impose for resolving disputes, such as exclusive forum requirements for Securities Act claims.

While many people will express views on whether a company should adopt a mandatory arbitration provision, the Commission’s role in this debate is to provide clarity that such provisions are not inconsistent with the federal securities laws. It will fulfill that role through the issuance of the Policy Statement.

Amendments to Rule 431 of the Commission’s Rules of Practice

In connection with the Commission’s vote on the Policy Statement, the Commission will also vote today on whether to amend rule 431[7] of its Rules of Practice,[8] which is the third item on today’s agenda. This rule governs the Commission’s review of actions made pursuant to authority delegated to its staff.

Since 1963, the Commission has delegated to the Director of the Division of Corporation Finance its authority to accelerate the effectiveness of a registration statement filed under the Securities Act.[9] I remember that in 2002, when I was confirmed as a Commissioner, a former Commissioner who served in the 1970s called to wish me the best, and one piece of advice that he gave me was not to spend a lot of my time reviewing registration statements, as he had done. My, how times have changed. Of course, this delegation is a practical necessity, as the Commission cannot possibly vote on the thousands of acceleration requests submitted each year. This is particularly the case with respect to market-sensitive transactions, where the Commission‘s delegation of authority to its staff to declare registration statements effective plays a critical role in the agency’s ability to move with alacrity on behalf of issuers and investors.

When the Commission acts via delegated authority, any individual Commissioner or any aggrieved person may ask the Commission to review that action.[10] Subject to limited exceptions, a request for review stays the prior action taken by delegated authority until the Commission orders otherwise.[11]

Currently, declaring a registration statement effective is not among the exceptions to a stay. However, stays of an effective registration statement may be extremely disruptive. A company, its underwriters, and other market participants may commence sales of the securities once the registration statement is effective. A stay of effectiveness could fundamentally interrupt the sales process. Investors – selling securities holders as well as purchasers — might be extremely disadvantaged. Market participants could incur costs as a result. A stay could also create uncertainty for issuers and underwriters that have sold securities. Rather than automatically trigger such adverse consequences, the Commission should have the opportunity to carefully weigh the equities involved before taking such a significant step.

Adding declarations of effectiveness of registration statements[12] to the limited list of exceptions to the automatic stay requirement will help to alleviate some of the aforementioned concerns. In the execution of its mission, the Commission should provide as much regulatory certainty as possible to market participants raising capital. Today’s amendments to rule 431 further that mission.

Conclusion

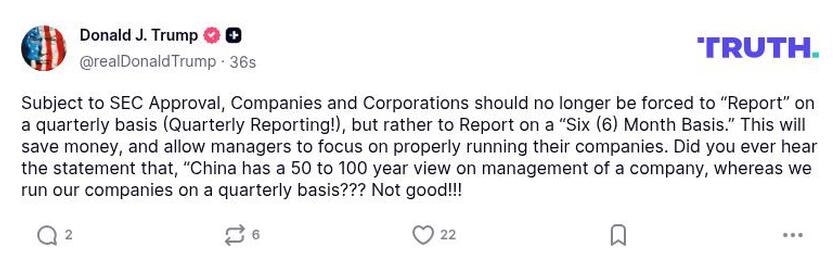

Today’s recommendations on mandatory arbitration and rule 431 are among the first steps of my goal to make IPOs great again. This ambitious project will make being a public company an attractive proposition for more firms by eliminating compliance requirements that yield no meaningful investor protections, minimizing regulatory uncertainty, and reducing legal complexities throughout the SEC’s rulebook. The next steps in this project include enhancing accommodations for newly public and smaller companies, expanding post-IPO companies’ ability to easily access the public markets to raise additional capital, simplifying disclosure requirements for executive compensation and other topics to focus on material information, and modernizing the shareholder proposal process.[13] I thank President Trump for his idea of semiannual reporting by public companies.[14] The staff is currently preparing recommendations for each of these topics, and I eagerly await the Commission’s proposal for each recommendation.

Before I turn the meeting over to Cicely LaMothe, Acting Director of the Division of Corporation Finance, to discuss the recommendations, I should note that Cicely will soon turn over her Acting Director duties to a permanent Director. As Acting Director, Cicely has done a wonderful job to keep the operations of the Division of Corporation Finance running smoothly, in addition to continuing to execute her “regular” responsibilities as Deputy Director of the Disclosure Review Program. She has helped to make my coming aboard as Chairman and my transition into this job a real delight. She and the staff have been very forward-thinking and creative in their advice to me. Cicely, I very much look forward to our continued collaboration in your very challenging role as Deputy Director, for which you are very well suited and have distinguished yourself.

Today’s recommendations on the Policy Statement and the amendments to rule 431 could not have been accomplished without the exceptional work of the following staff members:

- From the Division of Economic and Risk Analysis: Robert Fisher, Oliver Richard, Lyndon Orton, Angela Huang, Lauren Moore, Charles Woodworth, and Andrew Glickman;

- From the Office of the General Counsel: Jeffrey Finnell, Bryant Morris, Dorothy McCuaig, Brooks Shirey, Evan Jacobson, Michael Killoy, and Eduardo Aleman;

- From the Division of Investment Management: Brian Daly, Anna Sandor, Yoon Choo, Andrea Ottomanelli Magovern, Matthew Cook, and Jaea Hahn; and

- From the Division of Corporation Finance: Cicely LaMothe, Sebastian Gomez Abero, Michael Seaman, Jonathan Ingram, Adam Turk, Anna Abramson, Jessica Ansart, and John Fieldsend.

Now I will turn the meeting over to Cicely for the staff’s recommendations.

[1] Acceleration of Effectiveness of Registration Statements of Issuers with Certain Mandatory Arbitration Provisions, Release No. 33-11389 (Sept. 17, 2025), available at https://www.sec.gov/files/rules/final/2025/33-11389.pdf.

[2] See Section II.C of the Policy Statement.

[3] Brief for the Securities and Exchange Commission as Amicus Curiae Supporting Petitioners, Shearson/American Express, Inc. v. McMahon, 482 U.S. 220 (1987) (No. 86-44).

[4] See, e.g., Caryle Drops Arbitration Clause from I.P.O. Plans, Kevin Roose, The New York Times (Feb. 3, 2012), available at https://archive.nytimes.com/dealbook.nytimes.com/2012/02/03/carlyle-drops-arbitration-clause-from-i-p-o-plans/.

[5] See 8 DEL. CODE ANN. Tit. 8, Section 115(c) (2025) (effective Aug. 1, 2025). See also note 5 and accompanying text to the Policy Statement.

[6] See 15 U.S.C. 77h(a). The Commission must also consider “the public interest and the protection of investors” when accelerating effectiveness of registration statements. Id. As discussed in Section II.C.2 of the Policy Statement, mandatory arbitration provisions do not implicate this standard.

[7] 17 CFR 201.431.

[8] Amendments to the Commission’s Rules of Practice, Release No. 34-103980 (Sept. 17, 2025), available at https://www.sec.gov/files/rules/final/2025/34-103980.pdf.

[9] 17 CFR 200.30-1(a)(5). The Director of the Division of Investment Management possesses similar delegated authority to accelerate effectiveness of a registration statement under the Securities Act and the Exchange Act. See 17 CFR 200.30-5. For delegations of authority to the directors of the Commission’s divisions and offices, generally, see 17 CFR 200.30-1 – 200.30-19.

[10] See 17 CFR 201.430 and 17 CFR 201.431(e).

[11] 17 CFR 201.431(e).

[12] In addition to declaring registration statements effective, today’s amendments to rule 431 also include declaring post-effective amendments to registration statements effective and qualifying a Regulation A offering statement or a post-qualification amendment thereto.

[13] See Securities and Exchange Commission Agency Rule List – Spring 2025, available at https://www.reginfo.gov/public/do/eAgendaMain?operation=OPERATION_GET_AGENCY_RULE_LIST¤tPub=true&agencyCode&showStage=active&agencyCd=3235.

[14] @realDonaldTrump, Truth Social (Sept. 15, 2025), https://media-cdn.factba.se/realdonaldtrump-truthsocial/115208193218518172.jpg.

{kind=link}