INTRODUCTION

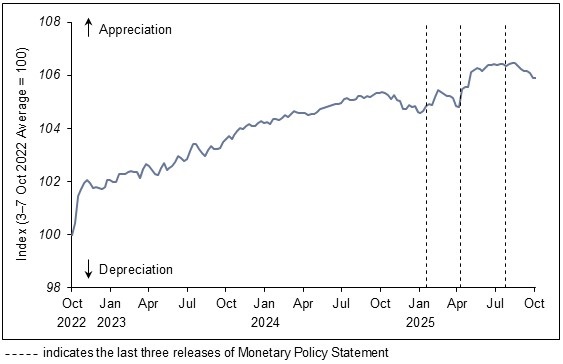

1. In its July 2025 monetary policy review, MAS maintained the rate of appreciation of the Singapore dollar nominal effective exchange rate (S$NEER) policy band, with no change to the width of the band or the level at which it was centred. After keeping close to the top of the policy band in August, the S$NEER has eased in recent weeks as appreciation pressures ebbed. On average, the level of the S$NEER since the July policy review has been similar to that in the preceding three months.

Chart 1

S$ Nominal Effective Exchange Rate (S$NEER)

GROWTH BACKDROP

2. The global economy has remained broadly resilient since the last monetary policy review. The staggered implementation of tariffs by the US has sustained the front-loading of shipments globally which, alongside robust AI-related investments, has buoyed manufacturing production and trade in Singapore’s major trading partners. In the quarters ahead, global growth should moderate as front-loading activity dissipates while labour markets soften and spending slows. However, the extent of the downturn should be contained. International production networks have demonstrated some flexibility in adapting to tariffs, while global financial conditions remain accommodative and supportive of investment, including in the IT sector.

3. Advance estimates from MTI today show that the Singapore economy expanded by 1.3% on a quarter-on-quarter seasonally-adjusted basis in Q3 2025, only slightly slower than the 1.5% recorded in the previous quarter. Growth surpassed expectations, underpinned by resilient activity in the manufacturing and domestic consumer-facing sectors. On a year-on-year basis, GDP growth came in at 2.9%, compared with 4.5% in Q2.

4. Singapore’s GDP growth is expected to moderate from this above-trend pace in the upcoming quarters as activity normalises in the trade-related sectors. However, continuing global investments related to AI will provide some support to the domestic manufacturing sector, while growth in construction and financial services should be bolstered by infrastructure investment and accommodative financial conditions, respectively.

5. The Singapore economy has expanded at an above-trend rate of 3.9% on a y-o-y basis in Q1–Q3 this year. MAS assesses that the output gap should stay positive for the year as a whole. In 2026, GDP growth is projected to slow in line with external developments to a near-trend pace, such that the output gap narrows to around 0%. The GDP growth forecasts for 2025 and 2026 will be announced in November by MTI.

6. Uncertainty around the economic outlook has receded somewhat with the conclusion of some trade deals between the US and various countries. MAS is monitoring closely the actual implementation of the tariffs, and the risks of renewed trade conflict and disruption. At the same time, further increases to effective tariff rates, including from product-specific duties, could impact the performance of Singapore’s externally-oriented sectors while still-elevated global policy uncertainty could also weigh more heavily on hiring and investments with a lag. An abrupt correction in the AI investment boom and the associated exuberance of financial markets is another downside risk to the growth outlook.

INFLATION OUTLOOK

7. MAS Core Inflation

8. While core inflation could edge down further in the near term, some of the factors dampening inflation are expected to diminish in the quarters ahead. Imported costs should exert a smaller drag on inflation in 2026, given projections for a more gradual decline in global crude oil prices, as well as a modest pickup in regional inflation from the easing this year. On the domestic front, services unit labour costs growth is projected to rise in 2026 as productivity growth normalises. Private consumption is likely to remain steady amid healthy household balance sheets and a broadly resilient labour market. The net drags on inflation associated with administrative price changes and their base effects should also unwind more discernibly from Q4 this year.

9. All in, MAS Core Inflation is forecast to trough in the near term and rise gradually thereafter. It should average around 0.5% for 2025 as a whole and come in between 0.5−1.5% in 2026.

10. CPI-All Items inflation, which fell to 0.6% in Jul−Aug, should average 0.5–1.0% this year. It is forecast to come in at 0.5–1.5% in 2026, with the anticipated pickup in core inflation offset to an extent by non-core components. Accommodation inflation is projected to ease as the more modest growth in market rents passes through to the CPI. Increases in private transport inflation should also be tempered by the further increase in COE supply.

11. The inflation outcome is subject to risks. Supply shocks, including those stemming from geopolitical developments, could lift some imported and shipping costs abruptly. Conversely, core inflation could stay lower for longer should growth be more hesitant and weaker than projected. Another significant decline in global oil prices could also temporarily tamp down the pace of price increases.

MONETARY POLICY

12. MAS has eased monetary policy twice this year. Singapore’s economic growth has turned out stronger than expected and the output gap will remain positive in 2025 and come in around 0% next year. MAS Core Inflation should trough in the near term and rise gradually over the course of 2026 as temporary factors dampening inflation fade.

13. MAS will therefore maintain the prevailing rate of appreciation of the S$NEER policy band. There will be no change to its width and the level at which it is centred.

14. MAS is in an appropriate position to respond effectively to any risk to medium-term price stability and will continue to closely monitor economic developments amid uncertainties in the external environment.

***

- [1] MAS Core Inflation excludes the costs of accommodation and private transport from CPI-All Items inflation.

Related: