INTRODUCTION

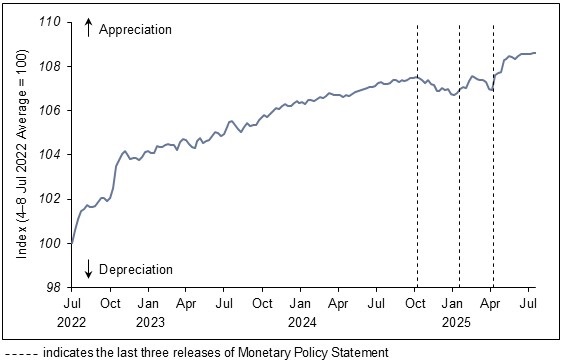

1. In its April 2025 monetary policy review, MAS kept the Singapore dollar nominal effective exchange rate (S$NEER) policy band on a modest and gradual appreciation path, but reduced its slope slightly. There was no change to the width of the band or the level at which it was centred. Since then, the S$NEER has strengthened toward the top of the policy band amid the broad-based depreciation in the US$.

Chart 1

S$ Nominal Effective Exchange Rate (S$NEER)

GROWTH BACKDROP

2. Since the last monetary policy statement, global economic growth has been more resilient than earlier anticipated. Worldwide manufacturing production and trade remained steady, supported by the front-loading of orders and continued AI-related investments. Over the rest of the year, growth momentum should moderate as front-loading activity dissipates, while the drags on demand exerted by policy uncertainty intensify, and previously delayed tariffs are implemented. However, the risk of a sharp step-down in global growth in the near term has receded along with the general de-escalation in trade tensions as well as more benign financial conditions since April.

3. MTI’s Advance Estimates showed that the Singapore economy expanded by 4.3% year-on-year in Q2 2025. Growth momentum was stronger than expected, registering 1.4% on a quarter-on-quarter seasonally-adjusted basis, a reversal of the –0.5% a quarter earlier. The robust performance was mainly driven by the trade-related cluster, even as the pace of expansion in several domestic-oriented sectors eased.

4. Singapore’s GDP growth is projected to moderate in the second half of 2025 from its strong pace in H1. In particular, the trade-related sectors should see some pullback, even as activity in the construction sector as well as segments within financial services are supported by a pickup in infrastructure investment and more accommodative financial conditions.

5. Prospects for the Singapore economy remain subject to significant uncertainty, especially in 2026. Changes in effective tariff rates worldwide could impact the performance of Singapore’s externally-oriented sectors. Renewed trade conflict, financial or geopolitical shocks would also exacerbate the drags posed by the global slowdown, and in turn weigh on domestic GDP growth.

INFLATION OUTLOOK

6. MAS Core Inflation

7. In the near term, inflationary pressures should remain contained. On the external front, ample global oil supplies and falling regional producer prices will tamp imported costs. Lower nominal wage growth and continuing increases in labour productivity will also dampen domestic unit labour costs.

8. MAS Core Inflation is projected to edge up slightly from the later part of 2025, as the disinflationary impact of enhanced healthcare subsidies introduced late last year, as well as that of the global oil price decline, tapers. For 2025 as a whole, MAS Core Inflation and CPI-All Items inflation are forecast to average 0.5–1.5%.

9. The inflation outlook in the quarters ahead is subject to both upside and downside risks. Geopolitical shocks could lift imported energy and shipping costs abruptly. Conversely, should global and domestic growth be more hesitant and weaker than anticipated, core inflation could stay low for longer.

MONETARY POLICY

10. The global and domestic economies have been resilient thus far. GDP growth in Singapore is expected to slow in H2, with the level of output falling slightly below potential. However, for 2025 as a whole, the output gap is projected to average around zero percent. Underlying inflationary pressures should remain contained in the near term. Given the uncertainties, MAS will closely monitor global and economic developments, and remain vigilant to risks to inflation and growth.

11. MAS will maintain the prevailing rate of appreciation of the S$NEER policy band. There will be no change to its width and the level at which it is centred. MAS had eased monetary policy twice earlier this year, and is in an appropriate position to respond to risks to medium-term price stability.

***

[1] MAS Core Inflation excludes the costs of accommodation and private transport from CPI-All Items inflation.

Related: