There are still a couple of weeks to go to submit your feedback regarding our Concept Paper on the creation of a New Board in Hong Kong aimed at attracting new economy companies. I won’t re-hash the entire paper here (you can read it or watch our webcast), but in a nutshell it proposes the establishment of a New Board with two segments: New Board PREMIUM would have roughly the same listing criteria as the Main Board today but allow companies with weighted voting rights (WVR), while New Board PRO would target early-stage pre-profit companies with light touch initial listing requirements and be accessible to professional investors only.

This is a Concept Paper by definition, so we are looking for thought leadership from the market and are open to any outcome. Meanwhile, a few issues have cropped up persistently over the last few weeks in my discussions with friends in the market, so I wanted to clarify our thoughts on them here.

1. Why would HKEX want to undertake such a major reform of the listing regime by creating the New Board?

We have a very good business model at the moment. We have traditionally had Chinese issuers and international investors, which is a great match. With Shanghai and Shenzhen Connect, we are now welcoming more Chinese investors with the goal of attracting more international businesses to list. With the four customers – Chinese issuers, foreign investors, Chinese investors and overseas issuers - we are in an advantageous position and it has driven our growth.However, that isn’t enough. Hong Kong has to “know its clients” and what they want, particularly future clients. If you look at the make-up of our market, it is overwhelmingly in traditional industries such as property and finance. But we’re in an unprecedented period of creativity and entrepreneurship that has created new industries, new sectors and new ways of business and life that we have never seen before. Hong Kong has to find ways to inject that new energy into our market and change its DNA. These creative and new economy companies represent the future and we have to make Hong Kong a welcoming home for these companies and their investors from China and everywhere else.

Our present listing regime isn’t agile enough to cope with the demands of this new age. This global relay race is in the first leg, and we are lagging behind; the good news is that we can still catch up if we do well in the second and third legs. After all, among global markets, only Hong Kong stands a chance at servicing all four of our customers well, which is a unique advantage of our market.

2. GEM didn’t work. Why are you confident launching another new board will?

There are a lot of opinions out there on GEM, but whether it’s perceived as successful or not shouldn’t prevent us from continuing to develop our market. If something didn’t work out before, it doesn’t mean we should give up and go home. If we never try, we will never be successful. But if we do try, we have a chance.

Some also wondered why we are at it again after our last consultation on WVR did not come to a fruitful conclusion almost three years ago. The answer is: things have changed a lot in the last three years; the world has moved on -- so has Mainland China and so has Hong Kong. Becoming a new economy market is too important an aspiration for us to shy away from reopening a debate no matter what the outcome might ultimately be this time around.

3. Hong Kong doesn’t really have a history of technology companies. How could the New Board succeed without a broader ecosystem?

We agree that Hong Kong still has some ways to go to be competitive in the new economy, but our market is competitively positioned given our unique connection between the world and China. We already have some of China’s largest and best new economy companies – some which are world leaders – on our markets. We have a good foundation but we have to begin earnestly building upon it rather than finding excuses why it can’t be done.

In that spirit, we plan to launch a completely new venture called the HKEX Private Market in 2018 to provide early stage companies and their investors with a share registration and transfer platform based on blockchain technology so they can conduct pre-IPO financing and other activities on an off-exchange venue not under the regulatory remit of the Securities and Futures Ordinance. The Private Market will serve as a “nursery” for early stage companies before they are ready to enter public markets. We are hopeful that the Private Market will help foster a welcoming and supportive ecosystem in Hong Kong for new, early-stage startups and their investors and form a critical mass for success.

4. What exactly is a “new economy” company? How will you be able to determine which companies qualify and which ones don’t?

It’s obvious that some companies will be considered “new economy”, such as those in technology, e-commerce, internet software and services, biotech and similar industries. It’s a broad concept and we expect it to evolve over time. The key principle is to identify companies whose businesses are in sectors where people rather than investment capital is the key, and creativity, innovation, technology, intellectual property, and new ways of commerce in totality are the primary drivers for its growth and business successes. Our plan is to work out a definition that is principle-based with feedback from the market.

If it’s anything like our listing suitability requirements, I anticipate that the overwhelming majority of the time it will be clear whether a company qualifies as “new economy”. It might be a bit murky in a small number of cases so we’d need to deliberate further. I’m sure we may not get it completely right all of the time, but that’s part of the learning process and I think the process will be refined and improved as we go along. It’s certainly no reason not to attempt this at all.

5. What if we just accept secondary listings from companies with WVR already listed in the United States? Wouldn’t that be easier?

The Concept Paper already proposes having New Board PREMIUM welcome secondary listings of US-listed firms with WVR structures, however there’s no reason to restrict WVR to only companies already listed on the US market. Hong Kong should be confident in its listing regime, as we have proven over many years that we have a robust and successful market. We should have confidence in our own vetting abilities, and not simply defer to the US market to make decisions on our behalf. We were confident enough to pioneer the H-share listing regime 20-plus years ago and start the mutual market access programme with the Mainland three years ago. There is no reason why we can’t accomplish what we set out to do without having to defer to or seek validation from someone else.

6. Why not just make changes to the Main Board to accommodate companies with WVR?

This is definitely something that can be considered, but I want to shed some light on why we proposed a New Board outside of the Main Board.

Our Main Board is the premier board in our market with rules and regulatory oversight that are clear to everyone. Any changes to this model, which has proven to be successful over the years, would require an in-depth consultation and would be a more controversial endeavour.

Imagine if a family wants to add a full-set of new, modern smart appliances to its existing kitchen. You could do it, but it would involve some big changes, be complicated and messy. Rather than cause such an inconvenience to the family, we propose building a kitchen extension so as not to disturb the family’s daily life. Once the new kitchen is done, we can enjoy having both or we can tear down the wall between them and have one large kitchen. But this is a decision that can wait for another day.

The important thing is to introduce a key new dynamic to our market with as little disruption as possible, but we are open to the best ideas for making it work.

7. New Board PRO is high risk, so why does it have a light touch initial listing regime? Isn’t that counter-intuitive? Could New Board PRO soon become a market of “listed shells”?

In an ideal world, we all wish that great companies could be allowed onto capital markets early on so that investors could benefit from their spectacular success while at the same time poor quality companies are barred from our markets through high hurdles and aggressive regulatory scrutiny. We do not, however, live in that ideal world. Nobody can tell in advance which companies will be great and which ones will turn out to be lemons. All great companies started as risky outfits in garages and basements and for every home run, there are dozens if not hundreds of strike outs.

If we do not want to miss the grand slam home runs, we have to make it easy for early-stage companies to access capital without making them spend limited valuable resources to work through a rigorous vetting and regulatory process. The only way to protect investors against such inherently high risk companies is either through full disclosure or, if still not sufficient, restricting access to professional investors only. This is a trade off that we all have to learn how to best assess.

Could New Board PRO potentially become another market of “listed shells”? No, it will be just the opposite. As listing on New Board PRO will be much easier, there would not be demand for the listing status or “shell” which would drain away much of its value as a tradeable commodity. We would also be focusing on the exit and looking at a more efficient delisting process, a system which wouldn’t allow zombie companies or "shell" companies to stay for too long. So we think easy-in and easy-out is the way to go for New Board PRO.

8. Is it fair to only allow professional investors to access New Board PRO, depriving public investors of the right to invest in future new economy stars?

There is no straight-forward answer to this question. It is a regulatory decision reflecting the market regulators’ philosophy and self-defined purpose. It is also a matter of how the regulators see the balance between investors’ freedom of choice and their need for protection.

Regulators of different markets adopt widely different approaches. A developed market like the US is a buyer-beware market, with the regulator stressing full disclosure and investors all treated equally. That means public investors do not enjoy more protective measures than professionals. On the flip side, in the retail-dominated Mainland market, Chinese regulators see themselves as having a mission to protect average people, so they have laid down elaborate mandatory measures including strict initial listing and post-listing criteria to protect individual investors. Hong Kong is a hybrid, in-between the US and the Mainland. It is a highly developed market but at the same time a market with a strong Chinese element. This is why we designed the current proposal for New Board PRO, restricting retail investors’ access to the higher risk market in order to ensure strong investor protection.

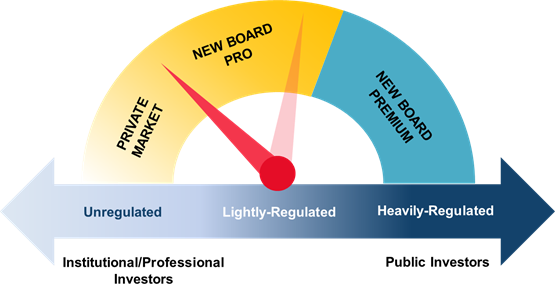

The bigger question we need to ask ourselves is this: what level of risk are we comfortable with as a market? If we break down our proposals, it spans a spectrum, as shown in the illustration below, from our private market, which is at the conception stage, is very high risk and involves very little or no regulation, to our New Board Premium which is a heavily-regulated board with stringent listing criteria and profits requirements, and is open to the public.

We can put ourselves anywhere along this spectrum: the further to the left we go, the more risk there is and the lighter touch that is required. For every iconic company developed this way, we might have many failures. If we aren’t comfortable with that, we can move along the spectrum towards the right, and slowly raise the barrier to entry and thus lower the risk.

There are pros and cons to each of the above approaches, and I think this is the framework in which we should be discussing how we want to position our market going forward. The proposals in the Concept Paper are a start, but the opinions from the market will be vital to developing a more diverse market that can serve the best interests of Hong Kong and remain globally competitive.

These are just a few of the questions that have come up, and I’m sure there are many more. We encourage everyone in the market to speak up and tell us what you think. The future of Hong Kong’s financial market depends on your participation.

We have spent many years considering how to strengthen Hong Kong as a financial centre while adhering to the city’s core values of fairness and investor protection. We have also considered many diverse points of view from different segments of the market. No solution is easy and without challenges, but doing nothing is not cost-free or risk-free either. Inaction does not eliminate risks and costs; it simply passes them on to the next generation. It is our duty to act and proactively make a decision in the best interest of the future of Hong Kong. That’s why it’s more important than ever that we work together and overcome obstacles to build a market that is well positioned to capture the next generation of opportunities.

Share your thoughts on Charles Li Direct with us. Email: ceo@hkex.com.hk. All emails sent to this address will be read, however, due to time constraints, the chief executive will be unable to respond personally to every email. If you have general enquiries or comments about HKEX, its products or services, please contact us through one of our usual channels. Thank you!