Judging from the recent strength in commodities and equities, markets seems to be anticipating a rapid “V” shaped recovery in the second half of this year, implicitly assuming little in the way of COVID-19 second wave effects. Sentiment now seems almost optimistic, especially about prospects for the rebound in China.

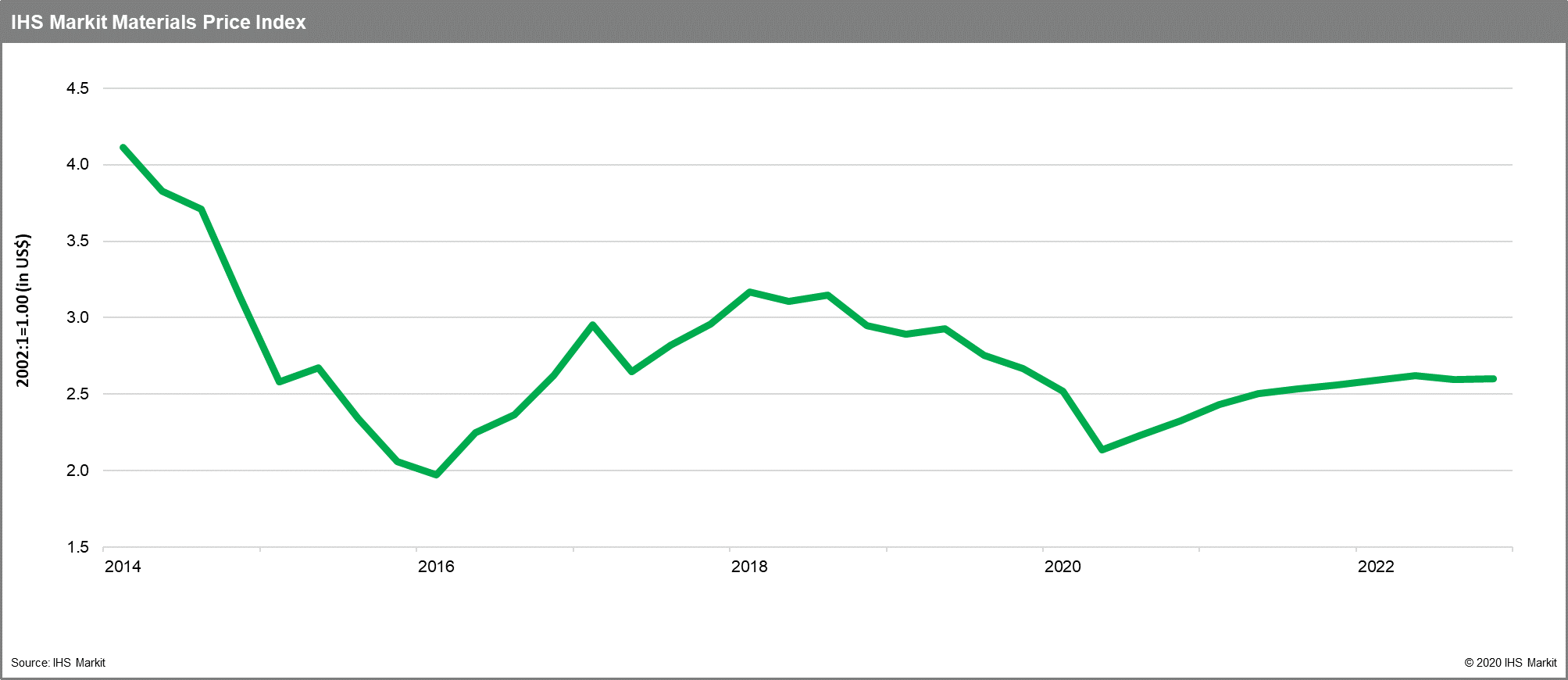

The IHS Markit Materials Price Index (MPI) has marked this change dramatically. After falling 28.5% across the first quarter, since bottoming in late April, the MPI has risen 21.6% in a strong seven-week run through mid-June.

To be sure, policymakers worldwide have provided extraordinary amounts of stimulus to support growth. Even so, the profound shock to both aggregate supply and demand caused by the global pandemic means that the recovery in global value chains is not likely to be rapid. Consumer spending and business investment are unlikely to return to ‘normal’ until a vaccine becomes widely available, which we assume is not until the second half of 2021.

“We expect a start-stop pattern to growth that translates into physical consumption returning to late 2019 levels sometime in 2022, which seems at odds with the strong rebound in commodity prices over the past seven weeks. It also seems at odds with the relative strength still seen in a safe-haven asset class like gold, or the lack of a lift in US bond yields. This points to a reckoning in commodity markets ahead, perhaps not an outright correction, but at least an end to the sustained increases seen since early May. The third quarter should prove interesting.” – John Mothersole, pricing and purchasing research director, IHS Markit

Commodity to watch: Copper

Copper prices have now staged an impressive two-month rally, with the LME benchmark price rising more than $1,000 to stand above $5,800 per metric ton. This strength reflects a combination of mine production cuts, a lack of scrap that is prompting buys of primary metal, and, most important, optimism over a stimulus-fueled revival in Chinese consumption. However, we believe the market has moved in front of fundamentals and has become exposed to a temporary correction.

The Materials Price Index (MPI) measures a weighted average of weekly spot prices for a key collection of globally traded manufacturing inputs. The components are crude oil, chemicals, nonferrous metals, ferrous metals, paper pulp, lumber, rubber, fibers, tech components, and ocean-going freight rates. It seeks to capture the commodity input costs for a diversified global manufacturer.